it refers to the money received for the hard work you have done.

Why do we need income?

We need income because it's the money we earn from our work or investments that allows us to pay for things we need and want in life. Income helps us buy food, pay for a place to live, cover our bills, and enjoy activities like going out with friends or taking vacations. It's like the fuel that keeps our lives running smoothly, helping us meet our daily needs and achieve our goals.

An individual may have several sources of income:

Wages/Salary earned from a job

Self-employment income earned from one's own business

Interest earned from savings a/c in bank

Rent earned from a property

Earnings from any investments made in stocks and bonds

It is important to have more than one source of income. If one source of income suddenly dries up or becomes unreliable, you can still rely on other methods to sustain yourself financially.

TYPES OF INCOME

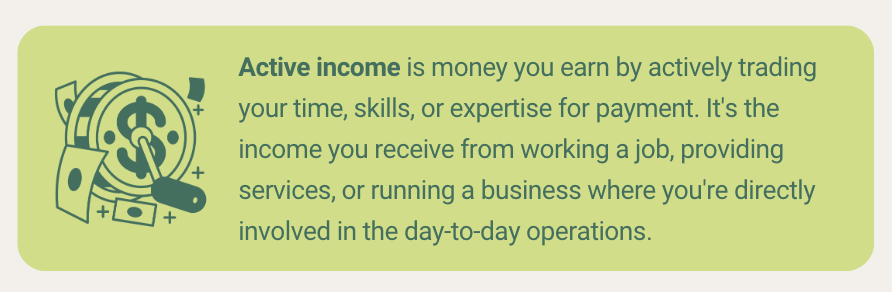

For example, if you work a regular 9-to-5 job, the salary or wages you

earn from that job is considered active income. Essentially, active income

requires ongoing effort and time investment to generate. Imagine you have

a job at a local bakery. Every day, you go to work and spend your time

baking delicious cakes, pastries, and bread. In return for your time and

effort, your boss pays you a salary or wages. This money you receive from

working at the bakery is an example of active income. To continue earning

income, you need to keep working at the bakery. As long as you're actively

working and contributing your time and skills, you'll receive your

paycheck.

Imagine you have a job at a local bakery. Every day, you go to work and

spend your time baking delicious cakes, pastries, and bread. In return

for your time and effort, your boss pays you a salary or wages. This

money you receive from working at the bakery is an example of active

income. To continue earning income, you need to keep working at the

bakery. As long as you're actively working and contributing your time

and skills, you'll receive your paycheck.

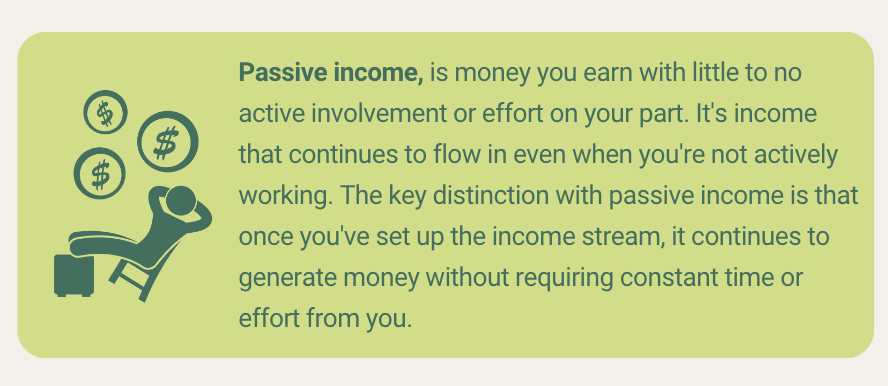

Imagine you own a rental property, like an apartment or a house. You've

rented out the property to a tenant, who pays you rent every month. The

money you receive from the rent is an example of passive income. Each

month, your tenant pays you rent for living in the property. While you

may need to handle occasional maintenance issues or communicate with

your tenant, the day-to-day management of the property doesn't require

constant active involvement from you. This money flows to you regularly,

providing a steady stream of income without requiring you to actively

work for it.

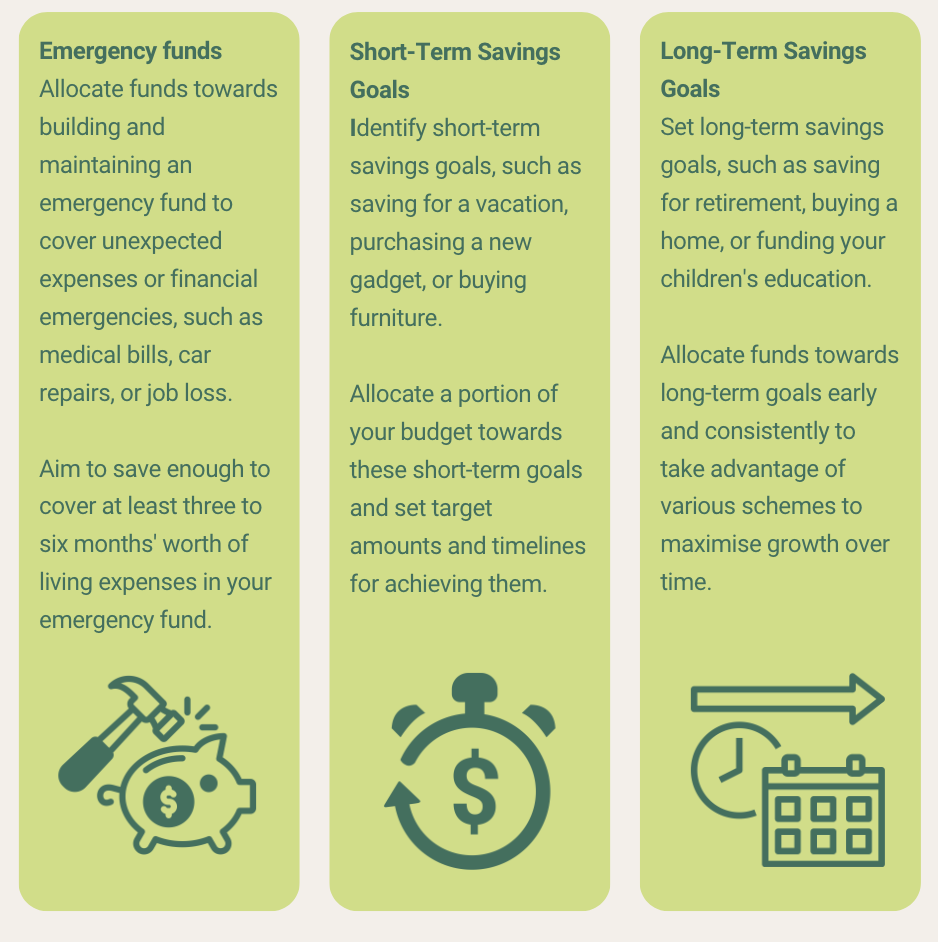

When budgeting, saving should be considered to ensure that you allocate funds effectively towards their savings goals.

For example:

Neha, a middle-class professional in her early 30s, works as a marketing

executive in a corporate firm. She lives in a rented apartment in a

metropolitan city with her husband and young daughter.

Neha's specific ambition:

Take her family on a dream vacation to Kerala, in six months' time.

She envisions spending quality time with her family amidst the

serene backwaters of Kerala. To fulfil this ambition, Neha aims to

save 5,000 inr per month for the next six months, totaling 30,000 inr,

specifically earmarked for the Kerala vacation.

In addition to her short-term goal of the Kerala vacation, Neha also

prioritises long-term financial security for her family. She aims to

allocate 5,000 inr per month towards retirement savings to secure her

future.

Income: Salary from Full-Time Job: 40,000 inr per month

Expenses:

Rent: 10,000 inr per month

Utilities (electricity, water, gas): 3,000 inr per month

Internet and Phone Bill: 1,500 inr per month

Transportation (commute to work): 2,000 inr per month